Walk through Canggu, Seminyak, Uluwatu or Ubud and you can feel two realities at once. On one side, Bali is busier than ever. The island welcomed around 16.4 million visitors in 2024, including 6.33 million international tourists, slightly above its pre-pandemic peak in 2019. In the first five months of 2025 alone, Bali recorded 2.64 million international arrivals, about 9% more than the same period in 2024.

On the other side, a growing number of villa owners and small developers quietly admit that their returns are under pressure. Rates are flat or falling, costs are rising, nights are harder to fill, and “for sale” signs are multiplying across real-estate platforms.

In short: Bali does not have a demand problem. It has a supply problem.

This article looks at the current oversupply of villas and short-term rentals in Bali, the numbers behind it, and what it means for:

- Existing villa owners and managers

- Would-be investors eyeing “passive” income

- Travellers choosing where and how to stay on the island

The punchline may be blunt but it is not hopeless: new villa investment in Bali requires extreme caution, but travellers and well-run, compliant operators can still come out ahead.

Tourism Demand in Bali is Still Strong and Growing

To understand the oversupply, it helps to start with demand. By most macro indicators, Bali tourism has fully recovered. Here are some statistics from Road Genius that prove it:

- In 2019, Bali received 6.28 million international visitors.

- International arrivals collapsed to almost zero in 2020–2021, then rebounded to 2.16 million in 2022 and 5.27 million in 2023.

- In 2024, total visitors (domestic + international) reached around 16.4 million, up roughly 7.9% from 2023.

- Early 2025 data shows 2.64 million international arrivals from January to May, already ahead of 2024 by about 9%.

Figure 1 – Bali International Tourist Arrivals, 2019–2025 (YTD)

Arrivals peaked at 6.28 million in 2019, collapsed during the pandemic, then rebounded to 6.33 million in 2024. Based on BPS and industry projections, Bali is on track to welcome around 6.7 million international visitors in 2025.

From a destination-wide perspective, this is a success story. Bali has bounced back faster than many competing islands. International exposure, digital-nomad content, and social media have all pushed awareness to new highs.

So if there are more visitors than ever, why are so many villa owners struggling?

The Truth: Supply Growth for Short-Term Rentals in Bali is Outrunning Demand

The simplest answer is that the number of villas and short-term rentals has grown even faster than arrivals.

Data from Airbtics, which tracks Airbnb markets globally, shows that between November 2024 and October 2025:

- Bali recorded 37,933 active Airbnb listings.

- The median occupancy rate was 65%.

- The average daily rate (ADR) was about IDR 1.53 million (around USD 94).

- The average annual revenue per listing was about IDR 326 million (around USD 20,000).

- Average monthly revenue fell by 6.13% year-on-year, despite strong visitor numbers.

Villa Finder’s own 2025 market session with owners and operators showed a similar pattern:

- International arrivals in Jan–Jun 2025 were up 13.9% year-on-year to about 3.3 million.

- Airbnb-style supply grew even faster, up around 18% year-on-year to roughly 39,000 listings.

- Average discounting increased from about 15% in 2024 to nearly 19% in 2025.

- Booking values fell by around 21.6% year-on-year.

That combination of more listings, deeper discounts, and lower booking values is textbook oversupply.

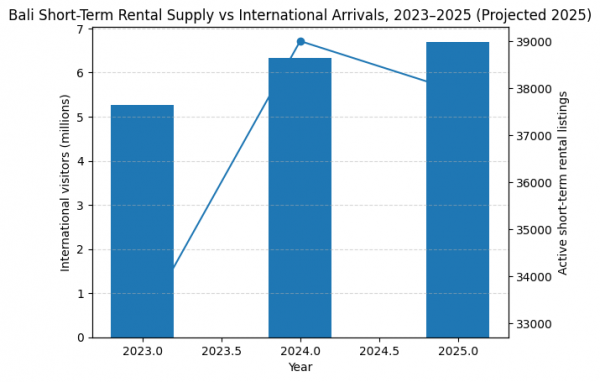

Figure 2 – Bali short-term rental supply vs international arrivals, 2023–2025.

Visitor numbers recovered strongly after the pandemic, but short-term rental supply has grown even faster, leaving owners to compete in a much more crowded market.

Independent Market Data Confirms the Oversupply

Across Bali, independent data sources put average short-term rental occupancy somewhere between 44% and 66%, with an average daily rate of around USD 93, depending on area and season.

In Canggu, one of the island’s hottest villa markets, some operators report year-on-year listing growth of more than 40% alongside declining occupancy, even though demand remains strong. In other words, tourism has recovered, but supply has multiplied faster, and owners are now competing in a far more crowded marketplace.

In other words: demand has recovered, but supply has multiplied faster. Owners are now competing in a far more crowded marketplace.

Hotels vs Villas: Oversupply in Bali is Not Evenly Distributed

It is important to note that Bali’s oversupply is not uniform across every type of accommodation.

Recent hotel and tourism statistics show:

- Overall star-hotel occupancy in Bali was close to 69% in mid-2024, with rising average length of stay and robust RevPAR growth.

- Industry reports and presentations suggest overall hotel occupancy in 2024–2025 sitting in the low- to mid-70% range, with around 58,000+ classified hotel rooms on the island.

From a hotel investor’s standpoint, the market looks tight but healthy. Many branded resorts continue to open or expand; for example, new high-end properties in Ubud and the Bukit peninsula are still coming online.

By contrast, the oversupply is most acute in unbranded, stand-alone villas and small clusters marketed through Airbnb and OTAs:

- Thousands of villas were developed quickly between 2022 and 2024, especially in Canggu, Berawa, Pererenan, Uluwatu and parts of Ubud, according to a report by Rumavi.

- Many of these properties share very similar layouts and aesthetics, which makes them interchangeable in search results.

- Only a fraction are managed with hotel-level revenue management, branding, and on-the-ground service teams.

The result is a two-speed market: branded hotels and integrated resorts have relatively strong pricing power, while generic villas fight over the remaining demand with discounts and upgrades.

The For-Sale Market: Thousands of Owners are Heading for The Exit

One of the clearest signs of oversupply sits not on Airbnb, but on the real-estate portals.

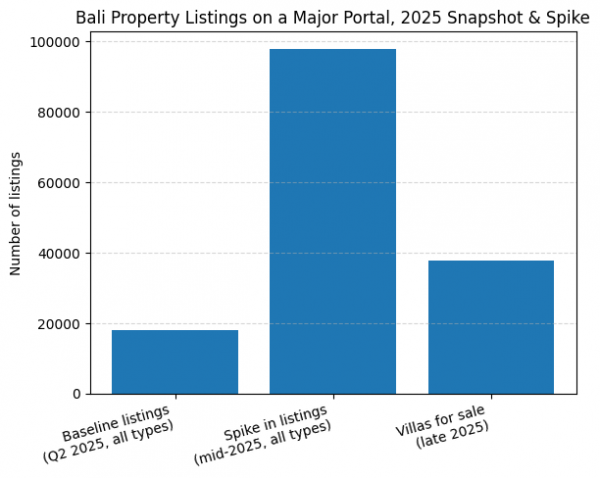

On one large Indonesian property portal, Rumah123, there were around 37,881 villas for sale in Bali as of late 2025. A separate analysis of listings on the same portal highlighted how total Bali property listings (all categories) surged from around 18,000 to nearly 98,000 in just a few months, driven heavily by villa stock coming to market.

Figure 3 – Bali Villas Listed for Sale on a Major Portal, 2022–2025

Total Bali listings on Rumah123 jumped from around 18,000 to nearly 98,000 within a few months, with roughly 37,881 of those being villas for sale — a clear sign that many owners and small developers are trying to exit.

The message is simple: many owners and small developers are trying to sell.

In parallel:

- Several advisory and property-investment firms caution that returns in saturated areas like Canggu and parts of Seminyak are under pressure, with more aggressive pricing needed just to maintain occupancy.

- Articles aimed at foreign investors increasingly stress regulatory risk and the need to move away from “set and forget” villa models toward integrated hospitality projects.

For investors who bought at peak land prices, financed construction in foreign currency, or underestimated operating costs, this squeeze can be painful.

Regulation Is Tightening: Unlicensed Villas Under Increasing Scrutiny

Oversupply is difficult enough on its own. Oversupply layered with a regulatory crackdown is a fundamentally different risk profile.

Since 2024, Bali has introduced or reinforced several measures:

- A tourist levy (around USD 9 per visitor) and a more explicit push toward “quality tourism,” acknowledging that mass numbers alone are putting severe pressure on infrastructure and the environment.

- A provincial task force to crack down on illegal foreign-owned or unlicensed tourism businesses, with a focus on villas and guesthouses operating without proper permits or tax compliance.

- High-profile actions such as the closure of the PARQ complex in Ubud and the demolition of dozens of cliff-side businesses at Bingin and Balangan, many of which lacked proper zoning or building permits.

- Intensified immigration patrols, including street-level document checks in hotspots like Canggu, Seminyak, Ubud and Uluwatu, targeting foreigners working or operating businesses illegally.

In late 2025, Bali’s governor floated a proposal to effectively halt or severely restrict daily rentals marketed through platforms like Airbnb from 2026, arguing that thousands of unlicensed villas erode hotel tax revenues and distort the market.

National authorities in Jakarta have since clarified that there will be no blanket ban on Airbnb or other OTAs, but platforms will be required to remove illegal listings and share data to support tax enforcement.

For fully compliant owners, this new environment is uncomfortable but manageable. For anyone operating in grey areas – nominee structures, incomplete permits, improperly zoned land, or undeclared income – the risk profile has shifted sharply.

In the medium term, however, stricter enforcement could actually be positive for operators who follow the rules. If platforms and regulators systematically remove non-compliant villas from the market, a sizeable chunk of today’s excess inventory could disappear. Even a reduction in the order of 30–40% of currently active but unlicensed stock would significantly ease oversupply and strengthen pricing power for genuinely legal, well-run properties.

How the Oversupply in Bali is Affecting Business Owners

Put the pieces together – strong arrivals, rapid supply growth, regulatory pressure – and the impact on villa owners becomes clear.

Margin Compression

Using Airbtics data as a rough benchmark, an “average” Bali short-term rental in 2025 looks roughly like this:

- Around 65% occupancy over the year

- An ADR of about IDR 1.5 million (around USD 94)

- Annual revenue in the region of IDR 320–330 million

- Average monthly revenue down just over 6% year-on-year

On its own, that does not sound disastrous. The problem is what sits on the cost side.

Owners are facing:

- Higher wages to attract and retain competent staff

- Rising utility and maintenance costs, especially for pools, generators, and air conditioning

- Increasing platform fees and performance marketing spend, simply to stay visible on OTAs and social

- Legal, licensing and accounting costs to stay compliant as the rules tighten

Layer on top of the fact that average discounts have climbed from around 15% to nearly 19%, and the conclusion is straightforward: many owners are working harder, investing more, and taking on more risk – for less net income.

Polarisation Between “Winners” and “Strugglers”

Oversupply does not hit every villa equally. It accelerates a split between those that operate like proper hospitality businesses and those that operate more casually.

Villas that continue to perform well tend to combine:

- Strong branding and professional photography, so they stand out in crowded search results

- Active revenue management, adjusting rates and minimum stays rather than “set and forget” pricing

- Clear positioning, such as family-first, wellness, digital nomad base, or retreat venue

- Consistently excellent reviews and on-the-ground service, which drive repeat bookings and referrals

- A complete guest experience, not just a nice pool and good Wi-Fi

On that last point, Jolien Keulen, Villa Finder’s Head of Distribution, sees a clear pattern:

“The villas that really hold their ground are the ones that include breakfast, offer add-ons like floating breakfasts and spa treatments, and invest in details like quality coffee machines, streaming services, and enough sunbeds for everyone. Guests feel they’re getting a full experience, not just a place to sleep.”

At the other end of the spectrum, the pressure is heaviest on:

- Generic villas in saturated micro-markets (for example, parts of Canggu, Berawa, Pererenan, and central Uluwatu)

- Properties with weak online presence or inconsistent management, where response times, photos, and guest communication fall behind competitors

- Owners who treat pricing and marketing as an afterthought, relying purely on location and aesthetics to do the work

As more owners chase the same pool of guests, rate wars become common. Travellers quickly learn that prices drop close to check-in, and last-minute discounting becomes the norm rather than the exception, further eroding perceived value and long-term pricing power.

Exit and Repositioning

The surge in for-sale listings suggests that a meaningful number of owners now see exit or repositioning as the rational response to oversupply.

Common strategies include:

- Selling at a modest profit or even at break-even, and redeploying capital into less saturated markets or different asset classes

- Converting short-term rentals into long- or medium-term leases for digital nomads or corporate tenants, trading higher potential yields for more predictable occupancy and cash flow

- Joining integrated hospitality projects, where individual villas sit within a branded resort or managed estate, sharing marketing, bookings, staffing and amenities instead of operating as stand-alone units

For investors who entered the market based on double-digit yield projections and minimal involvement, this is an uncomfortable reality check. However, acknowledging the shift – and adjusting strategy accordingly – is far safer than pretending Bali is still in its “any villa will do well” era.

How the Oversupply in Bali Affects Travellers

For travellers, Bali’s oversupply story looks quite different – and in many ways, more positive.

More Choice and Better Value

The most immediate upside of “too many villas” is choice.

In most popular areas, guests can now compare dozens or even hundreds of villas in the same price band. That depth of supply means it is often possible to secure larger spaces with private pools, kitchens and staff at effective nightly rates that were far harder to find a few years ago.

High competition and heavier discounting also make shoulder and low seasons particularly attractive for travellers who are flexible on dates. Where a family might previously have booked two hotel rooms, they can now often upgrade to a three- or four-bedroom villa with staff for a similar budget or a modest premium.

In short, oversupply has quietly shifted the value equation in favour of guests.

Greater Risk Around Quality and Compliance

The same forces that create bargains also introduce more risk.

Bali’s villa boom has included a wave of rapid, sometimes poorly regulated development. Not every property has been built or operated to the same standard. In practice, that can mean:

- Villas that do not meet robust structural, fire-safety or wastewater standards

- Properties operating without full business licences, tourism permits or tax registration

- Some villas being caught up in recent enforcement actions, with businesses around areas like Bingin and Balangan suddenly closed or demolished

For travellers, this changes the calculus slightly. The cheapest option is not always the smartest option.

How Travellers Can Use Oversupply Safely

Two practical guidelines help travellers benefit from oversupply without taking unnecessary risks:

- Favour reputable operators and vetted platforms.

Prioritise villas that are represented by established agencies or platforms that screen properties, verify permits where possible, and can provide support if something goes wrong – even if the headline rate is a little higher. - Treat extreme bargains with caution in saturated areas.

In markets already known for dense, rapid villa development, rock-bottom prices can be a signal of corners cut on build quality, safety, or legal compliance.

In an environment where enforcement is tightening, cheap but non-compliant increasingly means risky. Oversupply gives travellers more leverage and better value, but the safest way to use that advantage is to be selective about who you book with, not just how low the price goes.

Investment Outlook in Bali: Investors Needs to Exercise Extreme Caution; But There’s Still Opportunity if You Play It Smart

Given all of the above, is villa investment in Bali “dead”? Not necessarily. But the easy-money phase is over, and anyone buying into the market now has to be far more selective and realistic than in previous cycles.

What 2025–2027 Probably Looks Like

Over the next few years, several trends are likely to hold:

- Macro demand should remain strong.

Bali has already surpassed its 2019 international arrival numbers and still has room to grow domestic and regional traffic. The island’s brand remains powerful, and tourism is a core pillar of the local economy. - Oversupply will linger in saturated pockets.

In areas that have seen heavy villa construction – Canggu, Berawa, parts of Seminyak and Uluwatu – oversupply will probably persist until enough owners sell, repurpose, or are forced out by regulation. - Returns will become more polarised.

Differentiated, well-managed villas with clear positioning and strong operations can still perform. Generic, look-alike properties that compete only on price are likely to see thinner margins and more volatile cashflow. - Regulatory and immigration risk is structural, not temporary.

Authorities have signalled that enforcement against illegal or non-compliant businesses is here to stay. The direction of travel is toward more checks, more documentation and more pressure on informal operators, not less.

What Sensible Investors Should Now Look For

For anyone still considering a Bali villa investment, the filters need to be stricter and more disciplined. Sensible criteria include:

- Focusing on under-supplied or emerging areas.

Instead of piling into already crowded hotspots, target locations where supply growth is more controlled, demand drivers are clear, and planned infrastructure supports long-term tourism rather than short-term speculation. - Partnering with experienced, locally grounded operators.

Work with management teams that understand licensing, zoning, tax, staffing and guest expectations, and that already have proven distribution, pricing and review track records. - Stress-testing the numbers conservatively.

Model lower ADRs, slower occupancy growth and higher operating costs than the sales brochure suggests. If the deal only works on very optimistic assumptions, it probably does not work at all. - Accepting longer payback periods and uncertain capital gains.

Treat capital appreciation as a possible upside, not a given, and assume that recovering your investment will take longer than in the previous boom phase.

In short, Bali is no longer a market where buying any villa in any rice field and putting it on Airbnb is a sound plan. Oversupply and stricter regulation have turned it into a professional, data-driven game. Investors who approach it with that mindset still have opportunities; those who do not are likely to find the gap between expectation and reality uncomfortably wide.

How to Turn a Difficult Reality Into Something Useful

The conclusion is straightforward: Bali’s villa oversupply is real, and it is reshaping the island’s hospitality landscape in 2025.

- For business owners and investors, it means tighter margins, more competition, and the need for sharper positioning, better management, and full legal compliance.

- For travellers, it means more choice and value, but also a stronger need to choose vetted, professionally run properties.

If there is a positive angle, it lies in the fact that oversupply can force the market to mature.

Owners who adapt – by focusing on service, storytelling, guest experience, and compliance instead of just building another look-alike villa – will emerge stronger. Travellers who prioritise quality over the absolute cheapest rate will push demand toward operators who respect local regulations and communities.

And for Bali itself, painful crackdowns and difficult conversations about legality, zoning, and overtourism are part of the necessary work to protect the island’s long-term future.

As an investor, that means being brutally honest about the numbers and the risks. As a traveller, it means using your booking choices to support businesses that are doing things the right way.

Oversupply is the wake-up call. What happens next depends on how owners, guests, and policymakers respond to it.